When looking for immediate cash or a loan to help your business get the financing you need to start a project or build a product, there are a plethora of options available to you., but which one is right for you? Factoring vs. line of credit. What are the pros and cons of each? Where does a merchant cash loan fit into the equation? To start, they all vary in terms, costs, and payment structure.

When it comes to manufacturing businesses and companies that are making goods to be sold using accounts receivables or purchase order agreements for sales, Factoring is a hot term for a particular loan type. Factoring involves selling accounts receivable (unpaid invoices) to a third party (factor) at a discount. It’s more of a transactional arrangement than a loan. The factor purchases the invoices and assumes responsibility for collecting payments from customers. Factoring is typically used by businesses with slow-paying customers or those experiencing cash flow issues. The amount a business can receive from factoring is usually based on the value of its outstanding invoices and the creditworthiness of its customers who owe them the money.

Factoring vs. Line of Credit

Another popular business loan is a Line of Credit (LOC). A line of credit is a revolving loan facility that provides access to a predetermined amount of funds, which a borrower can draw upon as needed. Interest is only charged on the amount borrowed, and repayments restore the credit line for future use. LOCs are versatile and can be used for various purposes, including managing cash flow, financing inventory, covering short-term cash flow deficits, or covering unexpected expenses. Businesses often prefer them for their flexibility and ability to access funds quickly when needed.

Merchant Cash Advances (MCA)

Something we talk a lot about with clients and the entire network at Mobilization Funding is Merchant Cash Advances (MCA). These are loans you really need to be wary of. I have written a number of articles on these, and recommend you read about his more in detail here as well.

A merchant cash advance is a lump sum advance provided to a business in exchange for a percentage of its future sales or revenues. Unlike traditional loans, MCAs are repaid through a portion of the business’s daily credit card transactions or bank account deposits. MCAs are typically used by businesses with consistent credit card sales, such as retail stores or restaurants, and may be easier to qualify for than traditional loans. However, they can be expensive due to high fees and factor rates, making them less favorable for businesses, especially those with cash flow issues.

Cash flow comes in three forms: operating, investing, and financing. We’ll focus on operating cash flow, which is the money your business makes from selling goods or services. Basically, the money your company makes doing whatever it is your company does. Financial cash flow shows the money you use to fund your business, including debt, equity, and credit. Investing cash flow is money created from investment opportunities. Now let’s dive into the different types of cash flow and how to calculate operating cash flow!

Types of cash flow

There are three major sources of cash—operations (company revenue), investments, and finance (loans, lines of credit, equity raise).

Operations cash flow is all cash generated by the purchase of your company’s main service or product. Most of a typical contractor’s cash flow will come from operations, from the work you perform. When you bill your customers or submit a pay app and then get paid, that’s a primary source of cash. Consider if you have other sources as you prepare your cash flow statement.

Investment cash flow includes cash generated by investments in capital assets or other ventures. An example of this may be the interest charged on a loan to an employee or an investment made in another business, or it may be Bitcoin that you bought in the business.

Finance cash flow is the money you take in from debt or equity, less the payments you make on that debt or equity (known as “Debt Service”).

How to calculate operating cash flow

Let’s say you own a luxury baby apparel boutique and you have a goal to increase revenue by 25% as compared to the prior year. To reach that goal, you’ll want to estimate the necessary additional expenses and cash needs in order to make that goal attainable and then track against those estimates all year. You will also need a budget, but that is for another chapter. Follow the steps below on how to calculate operating cash flow or utilize a Cash Flow Calculator to streamline the process:

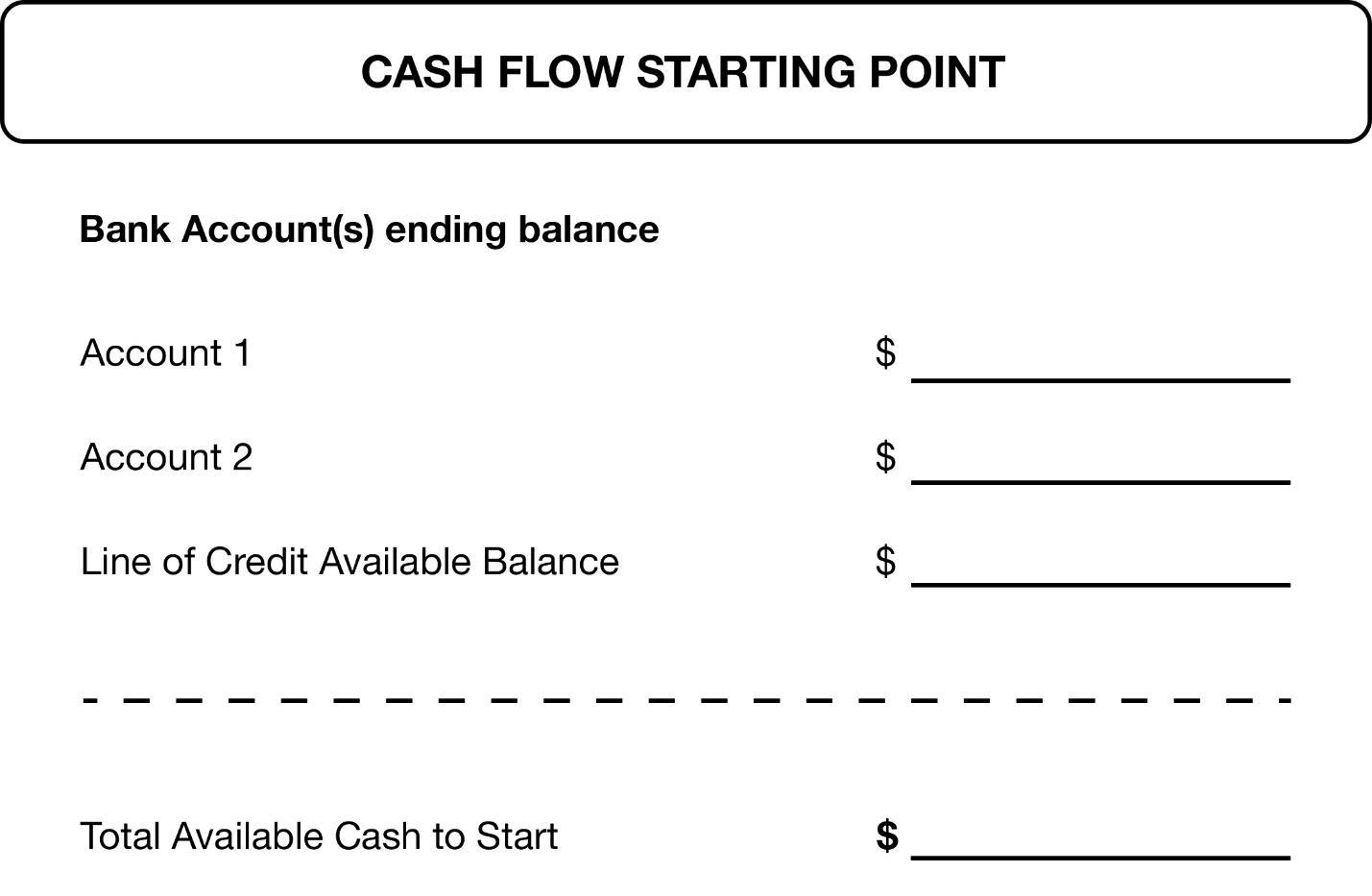

Step 1: Determine your cash flow starting point.

This is as simple as consulting your business cash flow report when you have one, but in the meantime, you will need to do a little work. Start with what is in your bank account(s) right now and add any additional sources of cash you have access to. Then add up all of the free cash flow from all other available Sources. This would likely be Operational cash flow. Next, you will need to choose a specific date to start from—oftentimes it makes sense to start with the end of the previous year because you should have a clean set of financials and/or a tax return that states specifically where you are at that period in time (December 31st). Then you can use that specific year as your “baseline” to project forward from.

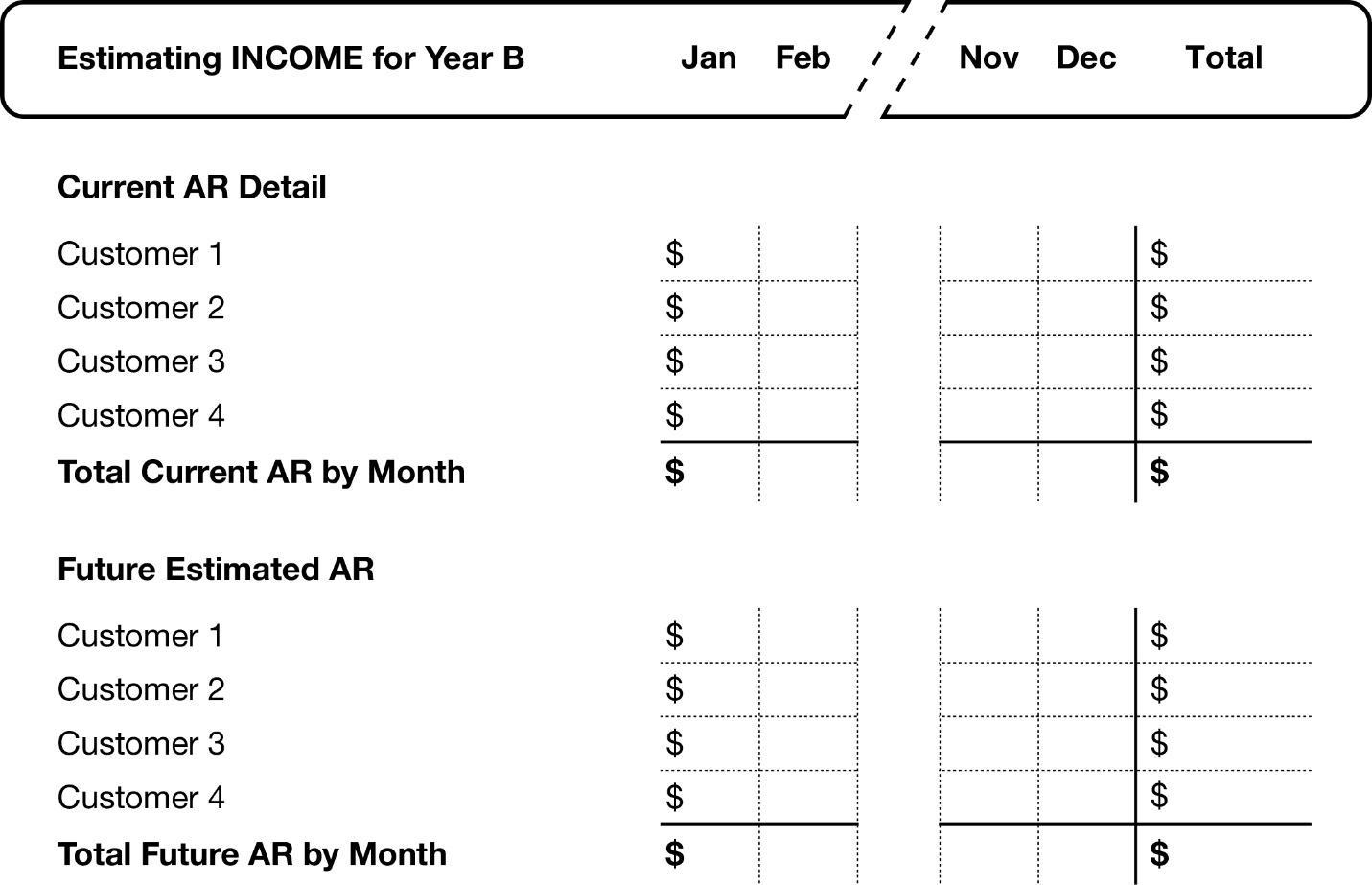

Step 2: Estimate incoming cash flow for the next period.

Based on historical cash flow tracking of Year A (the “baseline”), you can make a rough calculation of what the expected revenue will be for Year B.

Be sure to account for any anomalies, positive or negative, in the historical data. For example, if your company was closed for several months due to the shutdowns related to the coronavirus pandemic, that will have a negative effect on your cash flow data that should not be repeated.

Similarly, if you worked on a particularly large project—something way outside your normal scope—it is best to mark it as an outlier in terms of estimating cash flow. On the other hand, if you do have one-time events that you know are typical each year then you should account for those too.

For example, you are going to purchase a truck this year or you know one of your customers is going to order in bulk at the beginning of the year versus consistently every month like in previous years. These are the kinds of things to think about when planning in this stage of the process.

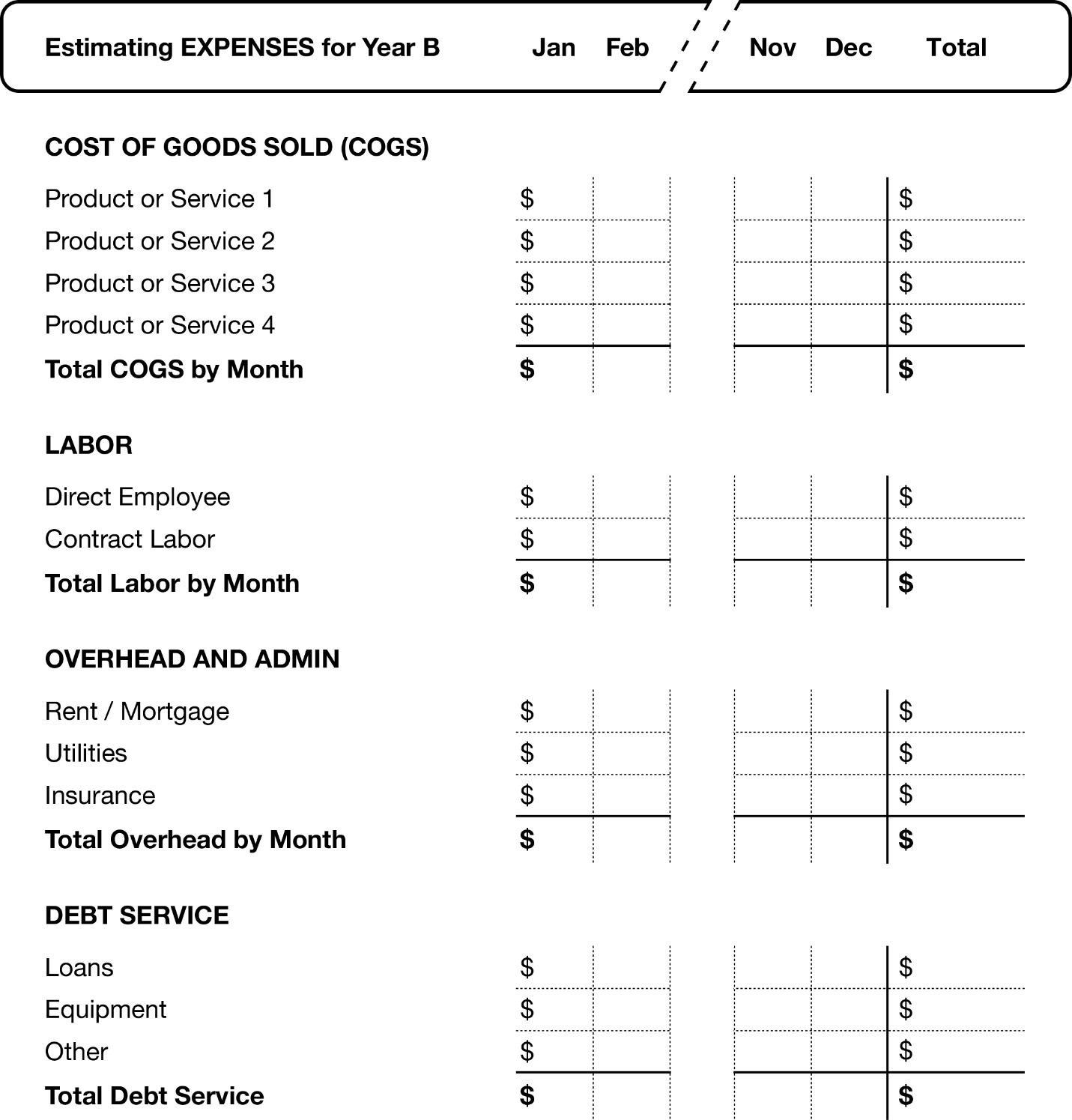

Step 3: Estimate outgoing expenses for the next period.

Just like you did with your revenue, you’ll want to review and tally up all of the expenses from the baseline period in order to get a rough idea of what you will spend in Year B. In a perfect world you will estimate revenue and expenses at least on a monthly basis to start and plan for the year—then refine this down to weekly looking ahead 13 weeks at a time. Then as each week goes on you add a week to the 13 so you always have a 13-week “look ahead” of the cash needs of the business. The week you finished becomes what actually happened and you adjust the weeks coming up and add one more week to the end. This allows you to always have a line of sight to the next 13 weeks of your business.

Step 4: Subtract the estimated expenses from the estimated revenue.

This one is pretty self-explanatory. Just like when you’re creating your cash flow statement, you need to subtract your expenses from revenue in order to arrive at your estimated free cash flow. This will give you the projected cash balance to end the period of time you are planning for.

Step 5: Estimate your starting and closing cash flow for the period.

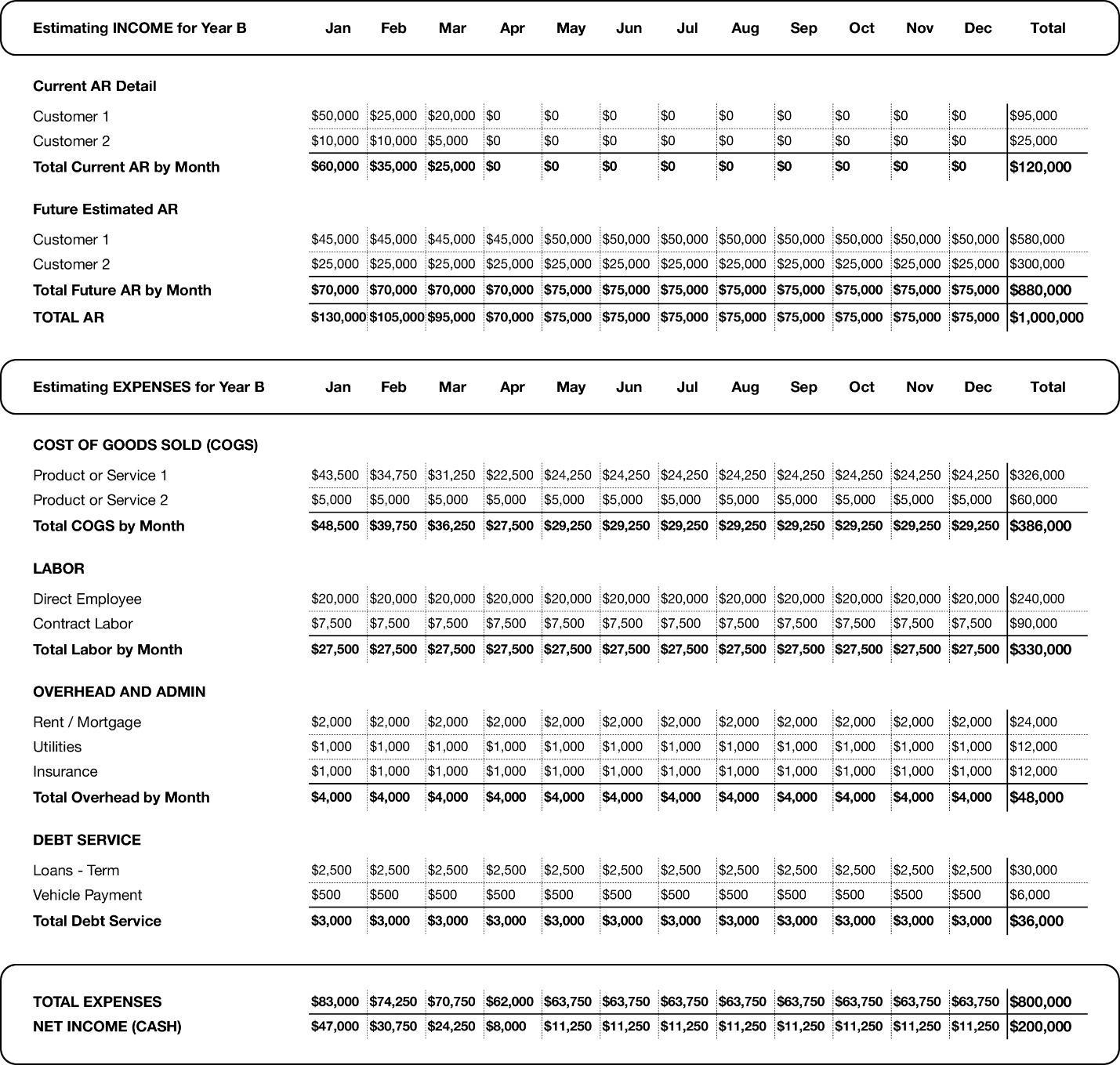

You can now see your estimated opening and closing cash flow statements for Year B. Let’s break it down in an example.

You ended Year A with an available cash flow balance of $250,000. Your Year B estimated revenue is 1,000,000. The estimated expenses for Year B are $800,000. Your estimated available cash flow is $200,000, and your closing cash balance is $450,000 ($250,000 from Year A and the additional $200,000 from Year B).

Now you have your starting point or opening balance and your estimate.

Estimating cash flow is not an exact science, especially when you are planning out an entire year. When you are looking at it yearly, that is more of a budget in our minds than a cash flow tool, but you need your budget to know where you are going to start from. Remember that these are your best guesses based on the data at hand. Stay flexible and regularly check in on your cash flow estimates as part of your cash flow management practices.

Consistently checking in on cash flow is something you want to do on a weekly basis, at a minimum, if not even daily. Again – we recommend you use a 13-week cash flow tool to manage the cash of the business. You can check out of free tool here. For more information and helpful tips, fill free to check out our Big Book of Cash Flow here and unlock your company’s potential for growth!

Congratulations on your new contract! “What are the project funding requirements?” is one of many common questions that arise as businesses begin to expand and grow. As businesses get multiple contracts at one time, analyzing and understanding your cashflow on each project becomes more important than ever before. First, you need to take a look at your cashflow (on each project and how they roll up overall to the whole company) to ensure you can first perform on the project and maintain or exceed the standards you have established for your team. Ask yourself these questions – do you have the labor force? Access to the suppliers you need? And, is the original plan when you bid on the project still in line today?

Next, get your financial reports in order – the last couple of business tax returns, bank statements for all business accounts, internal financial reports (income statement and balance sheet), debt schedule, Accounts Receivable (AR), and Accounts Payable (AP) reports. These are some of the main project funding requirements you’ll want to have available. Have these organized in one folder and spot you can easily access and send them to your lender when they ask for it. Include any Cash Flow modeling you have for the project and the amount you think you need to get the project done, how you determined that amount of money, and what you will be using the money for (this is commonly referred to as the “Uses” portion of a “Sources and Uses” report / spreadsheet / table).

You can also contact your existing relationships – bank and banker, accountant, controller, and colleagues in the industry. If you have not established relationships already for this exact purpose then you should contact the people you trust (friends, colleagues, and especially other business owners in your industry) and ask them who they use and their experience with them. Look at these options first, research them online, and see what they say about themselves and what others say about them. Do your research and homework on their website, YouTube Channel, and LinkedIn. See who resonates with you and contact those people first to see if they can help you.